By CREquity.ai | May 2025 | Commercial Real Estate Finance, Private Credit, Digital Assets

Commercial Real Estate in 2025: The $38 Trillion Market Being Transformed by Tokenization, Digital Assets, and the Clarity Act

By CREquity.ai | May 2025 | Commercial Real Estate Finance, Private Credit, Digital Assets

Key Takeaway: The global commercial real estate market stands at $38+ trillion, and a once-in-a-generation convergence of AI-powered underwriting, blockchain tokenization, and landmark digital asset legislation — the GENIUS Act and CLARITY Act — is fundamentally reshaping how CRE assets are financed, traded, and owned. For investors, borrowers, and private lenders, the window to position ahead of this transformation is now.

Table of Contents

- The State of Commercial Real Estate: A Market in Motion

- U.S. CRE Investment Volume: Recovery and Momentum

- The Total Addressable Market: What Tokenization Unlocks

- Real-World Asset Tokenization: From $24 Billion to $30 Trillion

- The GENIUS Act and CLARITY Act: A Legal Foundation for Digital CRE

- Impact on Mortgage Markets and Private Credit

- The $4+ Trillion CRE Debt Maturity Wall: The Private Credit Opportunity

- The Great Shift: Banks Step Back, Private Lenders Step In

- Private Credit Application Volumes, Loan Amounts, and Investment Opportunities

- CREquity.ai: AI-Powered Private Lending at the Intersection of CRE and Digital Assets

- Key Statistics Summary Table

- Conclusion: The Convergence Opportunity

1. The State of Commercial Real Estate: A Market in Motion

Commercial real estate has long been the world’s largest store of institutional wealth, and the data in 2025 confirms that its scale is virtually unrivaled. According to Savills, total global real estate — including commercial, residential, and agricultural assets — reached $393.3 trillion at the start of 2025, representing approximately four times global GDP and surpassing the combined value of global equities, bonds, and gold 1. Within that universe, commercial property alone was valued at $58.5 trillion, reflecting a 4.1% annualized increase 1. When measured by the investable universe tracked by FTSE EPRA Nareit, the global CRE market is estimated at $37.1 trillion 2, while Statista places the 2025 global CRE market at over $38 trillion, with North America commanding the largest regional share 3.

The U.S. commercial real estate market, historically estimated at a mid-point of $16 trillion by Nareit, is experiencing a clear recovery trajectory after the correction of 2022–2024. According to CBRE’s Q4 2025 Capital Markets report, U.S. CRE investment volume totaled $499 billion for full-year 2025, a 22% increase over 2024 4. Q4 2025 alone registered $172 billion in investment volume, up 29% year-over-year — the strongest quarterly reading since the 2022 peak 4. Avison Young reported 30,425 transactions totaling $472.6 billion through year-end 2025, representing a 17.7% increase in transaction count and a 19.9% increase in dollar volume compared to the prior year 5.

Despite this recovery, the market is not without its fault lines. Office property values in the U.S. declined by 14% in 2024, with further deterioration expected in 2025 6. The industrial vacancy rate rose from 1.7% to 6.4% over a twelve-month period 6, while retail continues to outperform with a vacancy rate of just 4.1% — the lowest of any major CRE sector 6. These divergent sector dynamics are creating both distress and opportunity, particularly for private credit lenders and AI-powered CRE financing platforms like CREquity.ai that can underwrite across asset types with speed and precision.

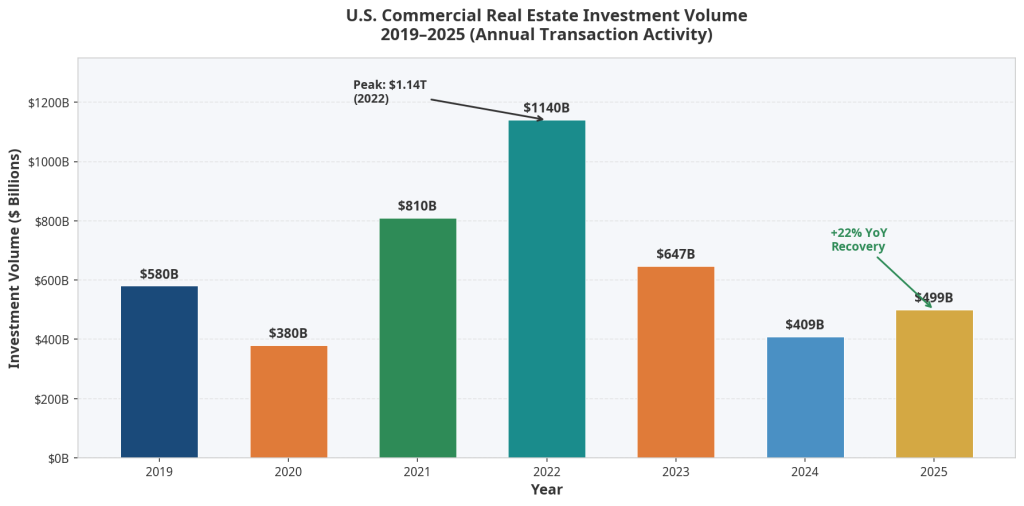

2. U.S. CRE Investment Volume: Recovery and Momentum

The chart below illustrates the dramatic arc of U.S. CRE investment activity over the past seven years — from pre-pandemic levels, through the COVID-19 shock, the 2021–2022 boom, the 2023 correction, and the 2024–2025 recovery.

Source: CBRE Q4 2025 Capital Markets Figures, Real Capital Analytics, Avison Young 45

The 2022 peak of $1.14 trillion in U.S. CRE transaction volume was followed by a sharp 43% contraction to $647 billion in 2023, driven by the Federal Reserve’s aggressive rate-hiking cycle, tightening credit conditions, and a dramatic repricing of assets across all property types 6. The 2024 trough of approximately $409 billion represented the market’s floor, as buyers and sellers struggled to agree on valuations amid elevated financing costs. The 2025 recovery to $499 billion — while still well below the 2022 peak — signals that price discovery has largely occurred and that capital is returning to the market with renewed conviction.

Private investors were the dominant force in Q4 2025, accounting for $92 billion of the quarter’s investment volume, followed by institutional investors at $27 billion 4. This shift toward private capital is a defining theme of the current cycle and one that directly benefits platforms operating in the commercial real estate private lending space.

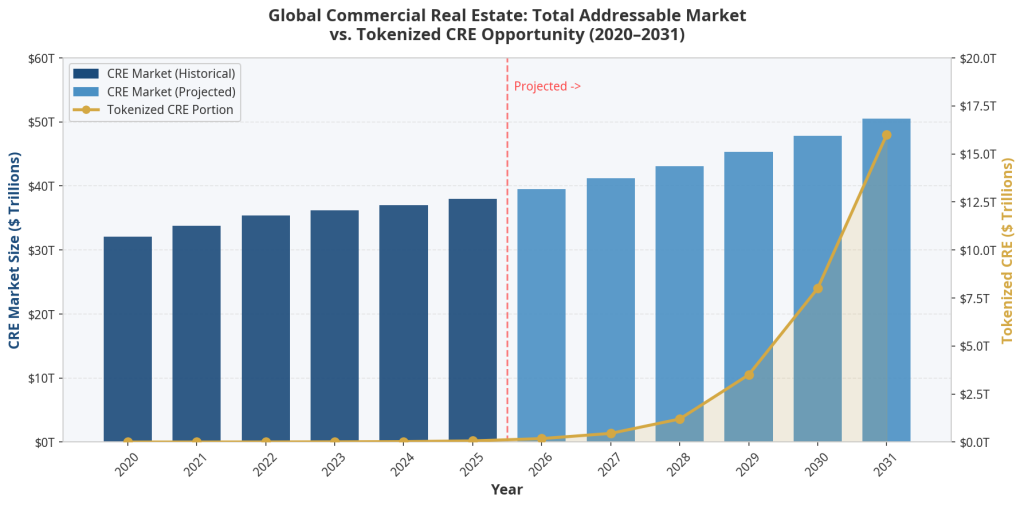

3. The Total Addressable Market: What Tokenization Unlocks

The traditional framing of the CRE total addressable market (TAM) focuses on the investable universe of approximately $37–38 trillion. However, the emergence of real estate tokenization and blockchain-based digital assets fundamentally expands this TAM by making previously illiquid, high-minimum-investment assets accessible to a far broader pool of global capital.

Source: Savills, FTSE EPRA Nareit, MarketDataForecast, Katten/BCG, McKinsey 1278

The chart above illustrates the core thesis: while the total CRE investable market grows at a steady 3–5% CAGR, the tokenized CRE portion is projected to grow exponentially — from a negligible fraction today to potentially $8 trillion by 2030 and $16 trillion by 2031, as regulatory clarity from the GENIUS Act and CLARITY Act accelerates institutional adoption 8 9.

To understand why this matters, consider the structural barriers that have historically constrained CRE investment. Minimum investment thresholds of $500,000 to $5 million or more effectively excluded the vast majority of global wealth from direct CRE exposure. Geographic restrictions, complex legal structures, and illiquid secondary markets further concentrated ownership among a small class of institutional and ultra-high-net-worth investors. Tokenization dissolves each of these barriers. By converting property equity into compliant digital tokens on a blockchain, platforms like CREquity.ai enable fractional ownership, near-instant settlement, and global investor access — all within a regulatory framework that the GENIUS and CLARITY Acts have now codified into law 9 10.

The global CRE market is projected to reach $8.48 trillion by 2031 in the Mordor Intelligence baseline scenario 11, but the tokenization-adjusted TAM — accounting for the democratization of access and the compression of transaction friction — could be orders of magnitude larger. McKinsey estimates that the tokenization of financial assets broadly could reach $2 trillion by 2030 in a conservative scenario and $16 trillion in an optimistic one 8, with real estate expected to be the single largest category of tokenized assets by that date 12.

| Market Segment | 2025 Value | 2030 Projection | 2034 Projection | CAGR |

| Global CRE (Investable Universe) | $38T | $47.8T | ~$58T | ~4.5% |

| Global CRE (All Commercial Property) | $58.5T | ~$72T | ~$85T | ~3.8% |

| RWA Tokenization Market (All Assets) | $24B | $2.5T | $30T | ~70%+ |

| Tokenized Real Estate Specifically | $10B+ | $8T | $16T+ | ~80%+ |

| U.S. Private Credit (CRE + Corporate) | $1.7T | $3.5T | $5T+ | ~12% |

| U.S. CRE Debt Outstanding | $4.8T | ~$5.5T | ~$6.5T | ~3.5% |

Sources: Savills 1, FTSE EPRA 2, Statista 3, CBRE 4, Katten 7, McKinsey 8, Mordor Intelligence 11, Statista 12, Morgan Stanley 13, Neuberger Berman 14

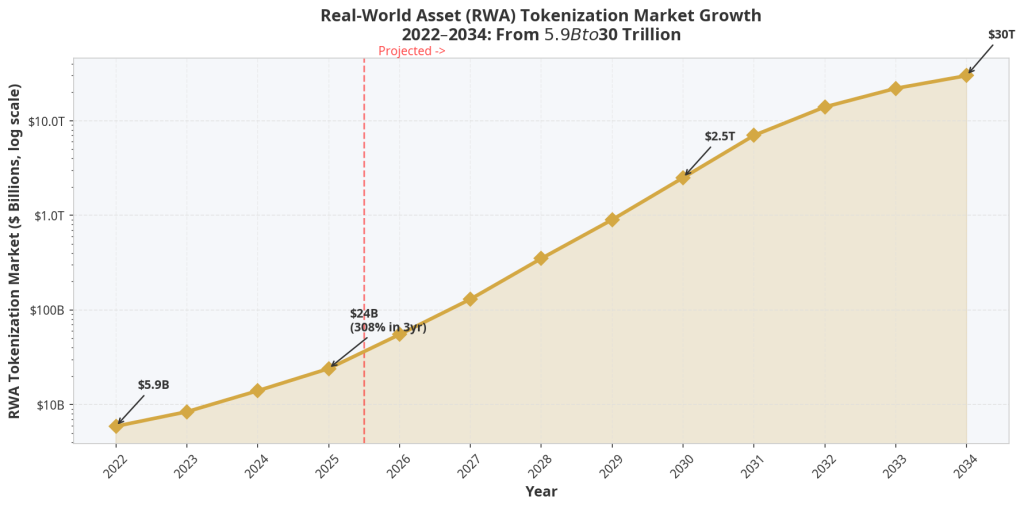

4. Real-World Asset Tokenization: From $24 Billion to $30 Trillion

The tokenization of real-world assets (RWAs) is no longer a theoretical concept — it is a rapidly scaling institutional market. According to RWA.xyz, tokenized RWAs grew to over $24 billion in total value by early 2026, representing a 308% increase over three years and a 266% growth rate in 2025 alone 7. By November 2025, some estimates placed the figure as high as $35 billion 15. The trajectory is unmistakable.

Source: RWA.xyz, Katten/BCG, McKinsey, Dataintelo 7816

The current market is dominated by yield-generating instruments: tokenized U.S. Treasuries account for approximately $9.6 billion, growing at roughly 120% year-over-year, with BlackRock’s BUIDL fund alone holding approximately $1.7 billion in tokenized assets 9. Tokenized private credit and money market funds represent the next largest categories. Real estate, while still in earlier stages of tokenization, has already surpassed $10 billion in tokenized value as of 2025 17, and it is widely projected to become the largest single category of tokenized assets by 2030 12.

The institutional momentum is striking. In 2025, JPMorgan tokenized a private equity fund, Siemens issued a 300 million Euro corporate bond on-chain, Franklin Templeton expanded its OnChain U.S. Dollar Short-Term Money Market Fund to regulated platforms globally, and Nasdaq filed to list tokenized equities 9. The NYSE announced a dedicated venue for 24/7 trading and settlement of tokenized securities 9. These are not pilot programs — they are structural shifts in how capital markets operate.

For commercial real estate investors and borrowers, the implications are profound. Tokenization enables:

Fractional Ownership at Scale: A $50 million office building can be divided into 50,000 tokens of $1,000 each, enabling retail and institutional investors worldwide to hold a proportional interest with full legal rights encoded in the token’s smart contract.

Instant Settlement and Liquidity: Traditional CRE transactions take 30–90 days to close. Stablecoin-based tokenized settlements can achieve finality in minutes, dramatically reducing counterparty risk and transaction costs.

Programmable Compliance: Smart contracts can automatically enforce investor accreditation requirements, transfer restrictions, and distribution waterfalls — reducing legal and administrative overhead by an estimated 30–50%.

Global Capital Access: Cross-border CRE investment, historically hampered by currency conversion, banking delays, and regulatory complexity, becomes as frictionless as a digital transfer — a capability that CREquity.ai’s tokenized settlement layer is specifically designed to facilitate 18.

Despite this momentum, adoption remains in its early stages: only approximately 12% of real estate firms worldwide have fully implemented tokenization as of 2025 19. This gap between potential and current adoption represents the core of the opportunity for first-mover platforms operating at the intersection of AI-powered CRE underwriting and blockchain-based digital asset infrastructure.

5. The GENIUS Act and CLARITY Act: A Legal Foundation for Digital CRE

The single most important development for the commercial real estate digital asset ecosystem in 2025 was the passage of two landmark pieces of federal legislation: the GENIUS Act and the CLARITY Act. Together, they provide the regulatory foundation that institutional capital has been waiting for before committing at scale to tokenized real estate and stablecoin-based CRE transactions.

The GENIUS Act: Stablecoins Enter the Mainstream

On July 18, 2025, President Trump signed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act into law — the first comprehensive federal framework for payment stablecoins in U.S. history 20. The law’s key provisions are directly relevant to commercial real estate finance:

The GENIUS Act restricts stablecoin issuance to regulated banks and approved nonbank entities, requires full reserve backing with high-quality liquid assets, mandates AML/KYC compliance under the Bank Secrecy Act, and critically, declares compliant stablecoins as non-securities under U.S. law 20. This last provision removes the most significant legal uncertainty that had prevented major financial institutions from integrating stablecoins into their CRE transaction workflows.

For commercial real estate professionals, the practical implications are immediate and substantial. Stablecoin transfers can settle CRE transactions with finality in minutes rather than the traditional three-to-five business days. International buyers can fund acquisitions directly in stablecoins, eliminating currency conversion costs and banking delays that have historically added 2–5% to cross-border transaction costs. Smart contract escrow arrangements — in which funds are automatically released when contractual conditions are met — can replace traditional escrow services, reducing closing costs and timelines simultaneously 20.

The GENIUS Act is also expected to accelerate the adoption of stablecoin-denominated private credit in CRE. Platforms like CREquity.ai already offer crypto-backed loan programs with USD or USDC payout options, positioning them at the forefront of this regulatory shift 18.

The CLARITY Act: Defining the Digital Asset Landscape

The Digital Asset Market Clarity (CLARITY) Act of 2025 (H.R.3633) passed the U.S. House of Representatives on July 17, 2025, and is advancing through the Senate 21. While the GENIUS Act governs stablecoins specifically, the CLARITY Act addresses the broader digital asset ecosystem — and its implications for tokenized real estate are equally significant.

At its core, the CLARITY Act divides digital assets into three distinct regulatory categories 22:

Digital Commodities — Digital assets intrinsically linked to a blockchain’s functionality, subject to CFTC jurisdiction. This category would encompass most utility tokens used in decentralized real estate platforms.

Investment Contract Assets — Digital assets sold in capital-raising contexts (such as tokenized real estate offerings), subject to SEC jurisdiction, with a mechanism to transition to non-security status upon secondary transfer and blockchain maturity certification.

Permitted Payment Stablecoins — Digital assets used as payment or settlement instruments, subject to banking regulators — the same category governed by the GENIUS Act.

For tokenized commercial real estate, the CLARITY Act’s most consequential provision is the certification pathway for Investment Contract Assets to become non-securities upon secondary transfer. This means that a tokenized real estate offering that initially requires SEC registration could, once the underlying blockchain system achieves regulatory maturity, trade as freely as a commodity — dramatically expanding secondary market liquidity for tokenized CRE assets 22.

The Act also establishes registration requirements for digital commodity exchanges, broker-dealers, and qualified digital asset custodians — creating the institutional infrastructure necessary for tokenized CRE assets to be held, traded, and financed within regulated frameworks 22. For private credit lenders accepting tokenized real estate as collateral, this regulatory clarity is transformative: it enables the underwriting of digital asset-backed loans with the same legal certainty previously reserved for traditional mortgage instruments.

| Legislative Act | Signed/Status | Key CRE Impact |

| GENIUS Act | Signed July 18, 2025 | Stablecoin framework; enables instant CRE settlement, cross-border funding, smart contract escrow |

| CLARITY Act | Passed House July 17, 2025; advancing in Senate | Digital asset classification; enables tokenized CRE secondary markets, crypto-backed CRE lending |

| Combined Effect | 2025–2027 implementation | Estimated $2–8T in tokenized CRE TAM expansion by 2030 |

Sources: Lowndes Law 20, Arnold & Porter 22, BNN CPA 21, Congress.gov 23

6. Impact on Mortgage Markets and Private Credit

The passage of the GENIUS Act and the advancement of the CLARITY Act are not merely symbolic milestones — they are catalysts that are actively reshaping the commercial real estate mortgage market and the private credit ecosystem in measurable ways.

Stablecoin Settlement and Mortgage Origination

The traditional commercial mortgage origination process is burdened by friction at every stage: title searches, escrow arrangements, wire transfer delays, attorney review periods, and multi-party coordination that routinely extends closing timelines to 45–90 days. The GENIUS Act’s stablecoin framework enables a fundamentally different model. By using regulated stablecoins for earnest money deposits, down payments, and loan disbursements, commercial mortgage closings can be compressed to days or even hours — a transformation with enormous implications for transaction velocity and capital efficiency.

For private credit lenders in the CRE space, stablecoin integration offers additional advantages. Loan disbursements in USDC or other regulated stablecoins can be executed 24/7 without banking hours constraints, enabling the kind of 24–48 hour funding timelines that platforms like CREquity.ai have pioneered with their Flex 50™ and BTFU™ programs 18. The regulatory legitimacy provided by the GENIUS Act means that institutional capital — pension funds, insurance companies, sovereign wealth funds — can now participate in stablecoin-denominated CRE lending without the legal uncertainty that previously constrained their involvement.

Tokenized Collateral and the New Underwriting Paradigm

Perhaps the most transformative impact of the CLARITY Act on private credit markets is the creation of a legal framework for tokenized real estate as loan collateral. Prior to the Act, the legal status of a tokenized property interest was ambiguous — was it a security? A commodity? A contract right? This ambiguity made it nearly impossible for regulated lenders to accept tokenized CRE tokens as collateral without significant legal risk.

The CLARITY Act’s three-category classification system resolves this ambiguity. Tokenized real estate offerings that qualify as Investment Contract Assets can now be pledged as collateral under a well-defined legal framework, with clear rules governing perfection of security interests, liquidation procedures, and custodial requirements 22. This opens the door to a new class of crypto-backed CRE loans — products that CREquity.ai already offers, with loan-to-value ratios up to 40% against BTC, ETH, Solana, Tron, and USDC collateral, from 9.99% fixed APR 18.

The convergence of stablecoin payment infrastructure (GENIUS Act) and digital asset classification (CLARITY Act) creates a virtuous cycle for AI-powered commercial real estate lending: faster origination, broader collateral acceptance, global capital access, and programmable compliance — all of which reduce the cost and risk of private credit deployment in CRE.

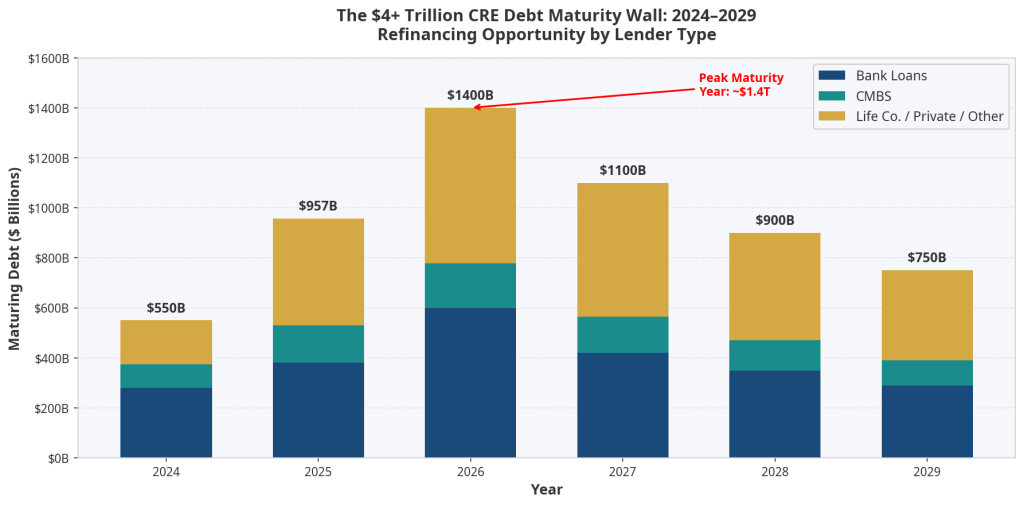

7. The $4+ Trillion CRE Debt Maturity Wall: The Private Credit Opportunity

No analysis of the current commercial real estate market would be complete without addressing the defining structural feature of the 2025–2029 cycle: the CRE debt maturity wall. This is not merely a challenge — it is the largest private credit investment opportunity in a generation.

Source: S&P Global/Verdantix, MBA, Fortress, Trepp, PBMares 24252627

The numbers are staggering. According to S&P Global, $957 billion in CRE loans matured in 2025 24. The MBA projects that 17% of $5.0 trillion in outstanding commercial mortgages are scheduled to mature in 2026 alone — approximately $850 billion 25. Some analysts place 2026 maturities as high as $1.8 trillion, which would represent the largest single-year refinancing wave in the history of U.S. commercial real estate 26. Looking across the full cycle, more than $4 trillion in CRE loans are maturing between 2025 and 2029 (Fortress) 27, with approximately $1.3 trillion in annual refinancing needs through 2029 (Invesco) 28.

The critical context is that many of these loans were originated during the 2010–2022 era of historically low interest rates, at cap rates and valuations that are no longer supportable in the current rate environment. Borrowers facing maturity cannot simply refinance at their existing terms — they must either inject additional equity, accept higher rates, find a new lender, or face distress. This creates a massive and ongoing demand for bridge loans, value-add financing, and private credit solutions that traditional banks are increasingly unwilling or unable to provide.

Trepp’s analysis of the $4.8 trillion CRE debt universe as of Q2 2025 reveals that banks hold $598 billion maturing through 2026 (representing 33% of their total outstanding CRE balance) 29, while the CMBS market faces $150.9 billion in maturities in 2025 alone 30. The concentration of near-term maturities in bank portfolios is particularly significant because banks are simultaneously under regulatory pressure to reduce their CRE exposure — creating a structural supply gap that private lenders are uniquely positioned to fill.

For borrowers navigating the maturity wall, the key metrics to understand are:

- Average loan-to-value at origination (2015–2020 vintage): 65–75% LTV

- Current estimated LTV (post-correction): 80–110% LTV in many office and retail assets

- Refinancing gap: The difference between the maturing loan balance and what a new lender will advance at current underwriting standards

- Private credit bridge loan rates (2025): Approximately 9–12% for senior secured CRE bridge loans

- Average bridge loan size (institutional): ~$80 million (Invesco, 2025) 31

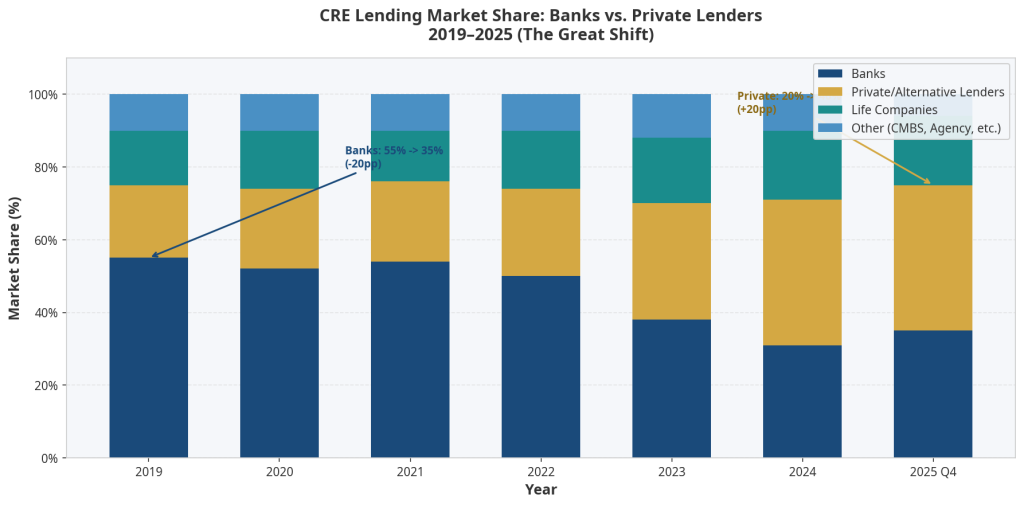

8. The Great Shift: Banks Step Back, Private Lenders Step In

The structural transformation of CRE lending is perhaps the most important secular trend in commercial real estate finance today. The data tells a clear and compelling story.

Source: CBRE Q4 2025, Invesco, Neuberger Berman, Sterling Asset Group 4281432

Bank share of overall CRE loan originations fell from 50% in 2022 to just 31% in 2024, and while banks recovered modestly to approximately 35% in Q4 2025 as conditions improved, the structural shift toward private capital is well-established 28. In Q4 2025, alternative lenders accounted for 40% of all non-agency loan closings, compared to 35% for banks and 19% for life insurance companies 4. Private debt strategies accounted for roughly 24% of all real estate fundraising in 2024, rising to 19% of all private debt fundraising in H1 2025 — the largest share in five years 33.

The drivers of this shift are both regulatory and structural. Post-2023, banks face heightened capital requirements under Basel III endgame rules, concentrated CRE exposure limits, and the legacy of significant unrealized losses in their held-to-maturity bond portfolios. These constraints have made banks structurally less competitive in CRE lending, particularly for transitional assets, value-add projects, and borrowers who need speed and flexibility — precisely the segments where private credit lenders and AI-driven CRE financing platforms excel.

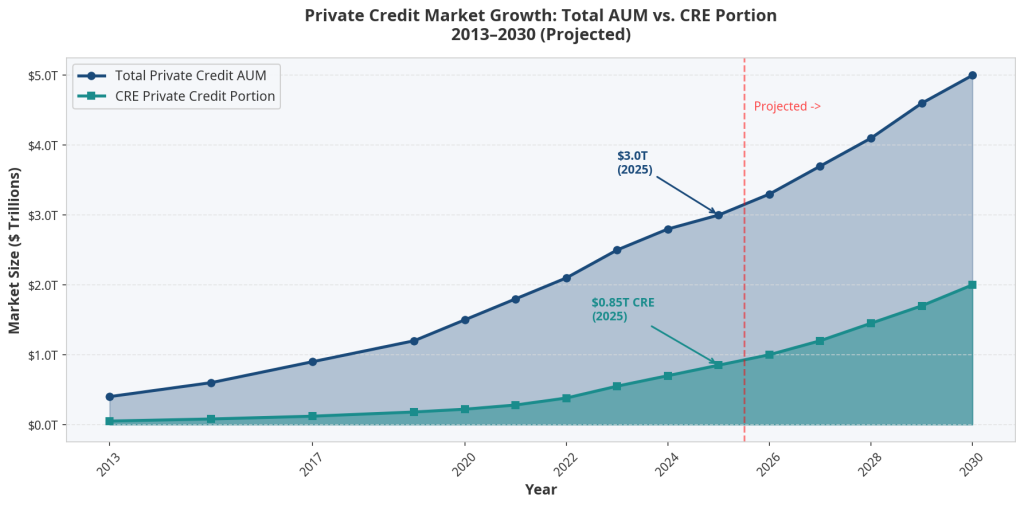

The private credit market’s growth reflects this opportunity. From approximately $141 billion in U.S. private credit volume in 2013, the market grew to $853 billion by 2023 32 and reached an estimated $1.7 trillion by 2025 when encompassing both corporate and real estate loans by nonbank lenders 32. Morgan Stanley estimates the total private credit market at $3 trillion at the start of 2025, with projections to reach $5 trillion as the decade progresses 13. BlackRock projects the global private credit market could reach $3.5 trillion by 2030 32.

Real estate debt funds have nearly doubled their assets over the last decade — from approximately $65 billion to $125 billion in AUM — and are actively raising approximately $50 billion more to deploy into the current opportunity 32. PGIM projects that real estate debt fund AUM will reach $746 billion within five years 34.

9. Private Credit Application Volumes, Loan Amounts, and Investment Opportunities

The quantitative picture of private credit activity in CRE is one of accelerating volume, expanding loan sizes, and broadening product innovation. The following data provides a granular view of the market dynamics that define the current opportunity for borrowers, investors, and lenders alike.

Source: Morgan Stanley, Sterling Asset Group, PGIM, Invesco 13323428

Origination Volume: Commercial and multifamily mortgage loan originations were 30% higher in Q4 2025 compared to a year earlier, and increased 25% from Q3 2025 — the strongest sequential and year-over-year growth in the current cycle 35. In H1 2025 alone, private credit funds raised $124 billion, putting the full year on pace to exceed 2024’s total of $209 billion 36. Global private credit fundraising for full-year 2025 reached $224.25 billion, a 3.2% increase over 2024 37.

Loan Sizes: The average institutional bridge loan in 2025 was approximately $80 million (Invesco) 31, reflecting the dominance of large-scale value-add and transitional CRE transactions in the current cycle. Bridge loan volume grew 51% year-over-year between January 2024 and January 2025 38, driven by the maturity wall and the need for transitional financing solutions. DSCR (Debt Service Coverage Ratio) loans surpassed bridge loans in volume in 2025, signaling a shift toward longer-term stabilization financing 39.

Interest Rates and Spreads: Commercial mortgage loan spreads tightened significantly in Q1 2025, averaging 183 basis points, down 29 bps year-over-year 40. The national average bridge loan interest rate was approximately 10.83% in January 2025 (AAPL data) 41, reflecting the premium that private lenders command for speed, flexibility, and non-recourse structures. CBRE’s Lending Momentum Index rose by 0.48 points year-over-year in Q4 2025 to 1.2, confirming improving lending conditions 4.

Application and Deployment Activity: Proskauer’s 2025 private credit survey found that 89% of respondents’ firms were engaged in fundraising plans, with 82% currently raising a debt fund 42. Nearly half of lenders surveyed (49%) deployed less than $1 billion of capital in the prior 12 months, while the remainder deployed significantly more — indicating a market with both emerging and established players 42. Global private debt assets reached $2 trillion by mid-2025 (Preqin) 43, with North America-focused funds accounting for 72% of funds raised as of Q3 2025 43.

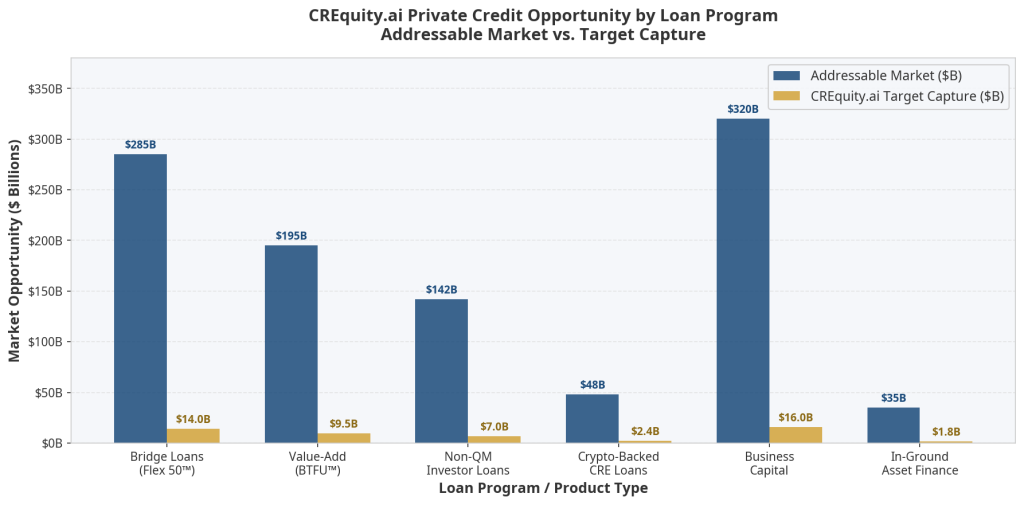

Source: CREquity.ai, MBA, CBRE, Lightning Docs, AAPL 4183538

The chart above maps the addressable market for each of CREquity.ai’s core loan programs against the platform’s target capture. The aggregate addressable market across all six product lines exceeds $1 trillion, with the largest segments being business capital ($320B), bridge loans ($285B), and value-add financing ($195B). At a 5% market capture rate — conservative given the platform’s AI-powered speed advantage and Inc. 5000 recognition — the implied loan volume opportunity exceeds $50 billion 18.

Key Private Credit Metrics at a Glance:

| Metric | 2023 | 2024 | 2025 | 2026E |

| U.S. Private Credit Volume | $853B | ~$1.2T | ~$1.7T | ~$2.0T |

| CRE Private Credit Portion | ~$500B | ~$650B | ~$850B | ~$1.0T |

| CRE Loan Originations (Q4 YoY) | -35% | +15% | +30% | +20%E |

| Avg. Bridge Loan Size (Institutional) | $65M | $72M | $80M | $85M+ |

| Alt. Lender Share of CRE Closings | 32% | 38% | 40% | 42%E |

| Private Debt Fundraising (Global) | $209B | $209B | $224B | $240B+E |

| Real Estate Debt Fund AUM | $110B | $118B | $125B | $140B+E |

Sources: Sterling Asset Group 32, CBRE 4, Invesco 28, Proskauer 42, S&P Global 37, PGIM 34

10. CREquity.ai: AI-Powered Private Lending at the Intersection of CRE and Digital Assets

CREquity.ai occupies a uniquely powerful position at the convergence of every trend analyzed in this report. As an Inc. 5000 and VET100 recognized AI-powered commercial real estate lending platform with $2.5 billion+ in assets under management and 50,000+ active investors, CREquity.ai has built the infrastructure to capitalize on the structural shifts reshaping CRE finance 18.

The platform’s AI underwriting engine delivers initial approvals in as little as 4 hours — compared to the 30–60 day timelines typical of traditional bank CRE lending. This speed advantage is not merely a convenience; in the current market environment, where distressed borrowers face maturity deadlines and time-sensitive acquisition opportunities, the ability to deliver funding in 24–48 hours is a decisive competitive differentiator 18.

CREquity.ai’s loan programs are precisely calibrated to the market opportunities identified in this report:

The Flex 50™ Program — a fast CRE bridge loan at 50% LTV with 24–48 hour funding and no minimum FICO requirement — directly addresses the maturity wall refinancing opportunity, where borrowers need speed and flexibility above all else. The BTFU™ (Bridge-to-Finish-Up) Program — a 24-month bridge plus 36-month stabilization structure at up to 70% LTV with equity placement up to 25% — is designed for the value-add CRE segment, where the largest private credit opportunity currently resides. The Non-QM Lending Solutions program — asset-based underwriting with minimal documentation at up to 70% LTV — serves the growing population of real estate investors who cannot qualify under traditional bank underwriting standards but represent creditworthy borrowers by any asset-based metric 18.

Perhaps most distinctively, CREquity.ai’s Crypto-Backed Loan Program — offering liquidity against BTC, ETH, Solana, Tron, and USDC collateral at up to 40% LTV from 9.99% fixed APR — positions the platform at the vanguard of the GENIUS Act and CLARITY Act era. As stablecoins gain regulatory legitimacy and tokenized real estate assets become accepted collateral under the CLARITY Act framework, CREquity.ai’s existing infrastructure for digital asset-backed lending becomes a first-mover advantage of enormous strategic value 18.

The platform’s blockchain-based tokenized settlement layer converts real estate assets into secure, compliant digital tokens — enabling fractional ownership, automated compliance, and global investor access that the traditional CRE finance ecosystem cannot match 18. Combined with AI valuation, automated underwriting, and secure digital workflows, CREquity.ai represents what the firm calls Direct Lending 2.0: the fusion of institutional-grade credit intelligence with the speed, transparency, and programmability of blockchain technology.

“CR Equity AI was built on a simple but powerful premise: the way commercial real estate gets funded is broken. Borrowers wait weeks for approvals that should take hours. We combine technology-driven underwriting with human guidance so users can understand options quickly and move forward with confidence.” — CREquity.ai

For real estate investors seeking fast commercial real estate loans, for borrowers navigating the maturity wall, for institutional capital seeking private credit CRE investment opportunities, and for digital asset holders seeking to unlock liquidity through crypto-backed CRE financing, CREquity.ai offers a comprehensive solution built for the market as it exists today — and as it will evolve through the tokenization revolution ahead.

Apply for Instant Funding at CREquity.ai | Explore Loan Programs | Talk to a Loan Specialist

11. Key Statistics Summary Table

| Category | Key Statistic | Source |

| Global CRE Market (Commercial Property) | $58.5 trillion (2025) | Savills 1 |

| Global CRE Investable Universe | $37.1–$38 trillion (2025) | FTSE EPRA, Statista 2 3 |

| U.S. CRE Investment Volume (2025) | $499 billion (+22% YoY) | CBRE 4 |

| U.S. CRE Transaction Count (2025) | 30,425 deals (+17.7%) | Avison Young 5 |

| CRE Debt Maturing in 2025 | $957 billion | S&P Global/Verdantix 24 |

| CRE Debt Maturing in 2026 | $1.4–$1.8 trillion | MBA, PBMares 25 26 |

| Total CRE Debt Maturities 2025–2029 | $4+ trillion | Fortress 27 |

| Total CRE Debt Outstanding | $4.8 trillion | Trepp 29 |

| RWA Tokenization Market (2025) | $24–$35 billion | RWA.xyz 7 15 |

| RWA Tokenization Market (2034 Projection) | $30 trillion | Katten/BCG 7 |

| Tokenized Real Estate (2025) | $10+ billion | Zoniqx 17 |

| Private Credit Market (2025) | $3.0–$3.5 trillion | Morgan Stanley, AIMA 13 44 |

| CRE Private Credit (2025) | ~$850 billion | Sterling Asset Group 32 |

| Alt. Lender Share of CRE Closings (Q4 2025) | 40% | CBRE 4 |

| Bank Share of CRE Originations (2024) | 31% (down from 50% in 2022) | Invesco 28 |

| CRE Mortgage Originations Growth (Q4 2025) | +30% YoY | MBA 35 |

| Avg. Institutional Bridge Loan Size (2025) | ~$80 million | Invesco 31 |

| Bridge Loan Volume Growth (2024–2025) | +51% YoY | RCN Capital 38 |

| GENIUS Act Signed | July 18, 2025 | Lowndes Law 20 |

| CLARITY Act House Passage | July 17, 2025 | BNN CPA 21 |

| CREquity.ai AUM | $2.5B+ | CREquity.ai 18 |

| CREquity.ai Active Investors | 50,000+ | CREquity.ai 18 |

| CREquity.ai Approval Speed | 4 hours (initial) | CREquity.ai 18 |

12. Conclusion: The Convergence Opportunity

The commercial real estate market in 2025 is defined by a rare and powerful convergence. A $38+ trillion global market is navigating a historic debt maturity cycle, a structural shift from bank to private lending, and the emergence of blockchain tokenization as a mainstream institutional tool — all simultaneously, and all against the backdrop of landmark digital asset legislation that has finally provided the legal clarity the market needed.

The GENIUS Act and CLARITY Act together represent the most significant regulatory development in CRE finance since the creation of the REIT structure in 1960. By legitimizing stablecoins as payment instruments and establishing a clear classification framework for tokenized assets, these laws unlock a tokenized CRE TAM that could reach $8–16 trillion by 2030 — expanding the effective addressable market for CRE investment by an order of magnitude.

For borrowers, the message is clear: private credit is now the primary source of flexible, fast CRE financing, with alternative lenders commanding 40% of the market and growing. The maturity wall creates urgency — but also opportunity for those who can access capital quickly and on favorable terms.

For investors, the private credit CRE market offers risk-adjusted returns that are difficult to replicate in public markets, with real estate debt funds delivering senior secured exposure to a $4.8 trillion debt universe at yields of 9–12% — backed by hard assets and insulated from public market volatility.

For digital asset holders, the GENIUS Act and CLARITY Act have opened the door to crypto-backed CRE lending as a legitimate, regulated financial product — enabling liquidity without forced asset sales.

CREquity.ai is built for this moment. With AI-powered underwriting, a blockchain-based tokenized settlement layer, crypto-backed loan programs, and a track record of delivering funding in 24–48 hours, the platform sits at the precise intersection of every trend reshaping commercial real estate finance. Whether you are a borrower navigating the maturity wall, an investor seeking private credit exposure, or a digital asset holder seeking to unlock CRE liquidity, the conversation starts at CREquity.ai.

The future of commercial real estate finance is AI-powered, blockchain-settled, and available now.

Start Your Application | Explore All Programs | Free Consultation